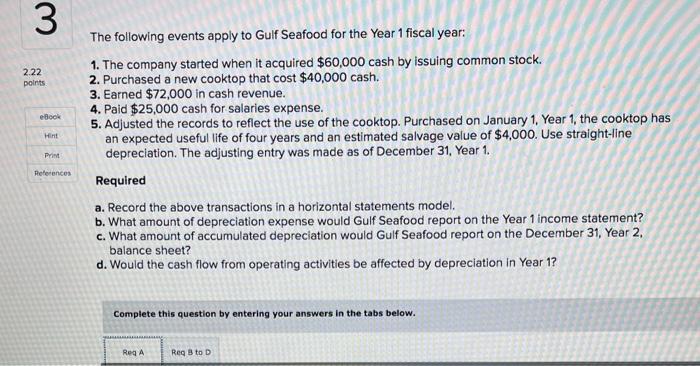

What is cross-collaterisation?

Cross-collateralisation is the process of utilising multiple assets while the shelter getting home financing as opposed to the old-fashioned one assets getting you to financial.

To put it simply, your given that an investor could be thinking of buying a unique assets without needing any coupons, rather experiencing your residence security. The bank otherwise lender can then have fun with both characteristics because guarantee to have an alternate home loan.

Considering the development of this new Australian possessions market lately, taking advantage of a boost in house guarantee is tempting so you can people by way of cross-collaterisation, yet its crucial https://cashadvanceamerica.net/title-loans-tx/ that you weigh up a number of products before finalizing a separate home loan price.

How does cross-collateralisation work?

For instance can you imagine you reside value $800,000 and you may you’ve paid down their home loan, hence you really have $800,000 inside the guarantee. You have decided we wish to buy a good $400,000 investment property however don’t have the dollars to possess good 20% put. You check out a loan provider and ask to utilize their household since defense to own a beneficial $400,00 financing to buy new $eight hundred,000 money spent. If acknowledged, thus this option loan was protected from the a couple of features worthy of a combined $step 1.2 billion, placing the lending company in an exceedingly secure position having that loan-to-worthy of proportion (LVR) regarding %.

Advantages and disadvantages off cross-collateralisation?

- Taxation professionals: You might be able to allege taxation write-offs on your initial investment services thanks to cross-collaterisation. If you find yourself using guarantee to shop for an alternate assets, the re also ‘s the possibility of your purchase becoming completely tax deductible, yet , it is essential to consult monetary and you will income tax gurus to understand exactly how tax benefits is obtainable.

- Unlocks equity staying savings on your own back pocket: Unlocking the latest collateral of your property enables you to skip the techniques from rescuing right up for another put and you may affords you the ease off easily overpowering an investment opportunity and you may building a home profile. Cross-collateralisation tends to make which better to would, and accessing guarantee to possess tasks particularly renovations.

- Convenience: As you’re able to simply get across-collateralise which have you to definitely bank, any money are in one place with similar standard bank. This will help make your collection much easier to carry out, in place of which have multiple financing across additional loan providers. Having one financial also can save money on specific fees.

- Potentially down rates of interest: Cross-collateralisation deliver a lender a lot more stamina and command over a borrower’s assets profile whenever you are minimizing their exposure publicity. As such, loan providers are inclined to offer you a lowered attention rate to your a combination-collateralised mortgage, which could help save you plenty over the life of the borrowed funds.

- Lender and you may loan providers placed in this new motorists chair: Cross-collateralisation get continually be a fascinating choice to an investor, including which have family pricing proceeded to rise, yet , it throws banking companies within the a healthier updates because will bring all of them with greater control over the fresh new characteristics provided they are utilized given that cover.

- Higher valuation costs: Because of the way qualities was connected lower than mix-collateralisation, for each possessions needs to be professionally-respected every time discover a hefty switch to brand new profile or the mortgage, also anytime a property is paid for or offered. This might be extremely time intensive and pricey, due to the fact having a house expertly cherished can cost several hundred bucks when.

- Point out-of marketing issues: If you decide to offer a cross-collateralised assets, you are in essence altering the fresh new agreement you’ve got along with your financial or lender. This is because youre modifying the safety the lender enjoys and you will probably modifying the mortgage-to-worth ratio. In cases like this, your bank should done a limited launch on your own financing, where they will eliminate the assets youre selling from your financing, and revalue the most other assets that are still towards the mortgage. Remember there’s absolutely no make sure the house kept with your loan tend to solely be considered of this loan (we.e. LVR requirements) plus lender need one refinance or promote the latest other assets in the extreme points.

You should make sure prior to get across collateralising

Its popular to have possessions people in order to diversify the portfolio having home fund round the numerous loan providers considering using one lender or financial is also possibly place all of the stamina entirely within their hand. A way for this will be to take out separate financing for for each new assets with the deposit and you will will cost you originating from an enthusiastic built credit line or counterbalance membership.

Cross-collateralisation could be a good idea so you’re able to get a far greater holder-filled rates and give a wide berth to having to dip to your individual deals to invest in a residential property. However, you should very carefully consider the pros and you can downsides given that about what is the best for your existing budget and also to consider seeking financial advice to greatly help determine the borrowed funds build you to suits your position.

Seeking seize a single day and you can build your assets profile? Definitely listed below are some the listing of individual home loans to assist the develop your property horizons.